For those who are unfamiliar, Opendoor (OPEN) is the world’s largest iBuyer. The company uses technology and data science to buy homes from sellers virtually. It then turns around and uses that same approach to sell those homes to prospective buyers.

We love this business model. We think it’s genius. It dramatically improves the archaic, universally-hated home-buying model. Specifically, Opendoor makes the home-shopping experience:

- Cheaper – it axes profit-taking middlemen (real estate agents) and replaces their often-flexible 6% commission with a 5% flat transaction fee.

- Faster – Opendoor’s advanced data science methods accurately price a home in minutes. And sellers can close a sale in as few as three days.

- Easier – Opendoor allows folks to literally sell their home from their mobile phone with just a few clicks.

- Simpler – Opendoor simplifies home-selling into a unified process between just the seller and Opendoor. Say goodbye to disjointed and complicated sales between multiple parties.

- More convenient – Opendoor allows sellers to choose their closing dates and escrow periods, enabling the flexibility to move on their own time.

- More reliable – Opendoor’s offers are all-cash. And its transactions never fall through because it “fails to qualify” – something that happens quite often in the home-selling process.

From a consumer advantage perspective, Opendoor is creating a superior way to buy and sell homes. It’s the future of home shopping. By 2030, we believe a large majority will use Opendoor to buy and sell homes. It’ll be much the same way shoppers today use Amazon (AMZN) to buy goods instead of going into Walmart (WMT) or Target (TGT).

To that end, we see Opendoor as an early stage “Amazon of Houses.”

Don’t Worry About Profitability

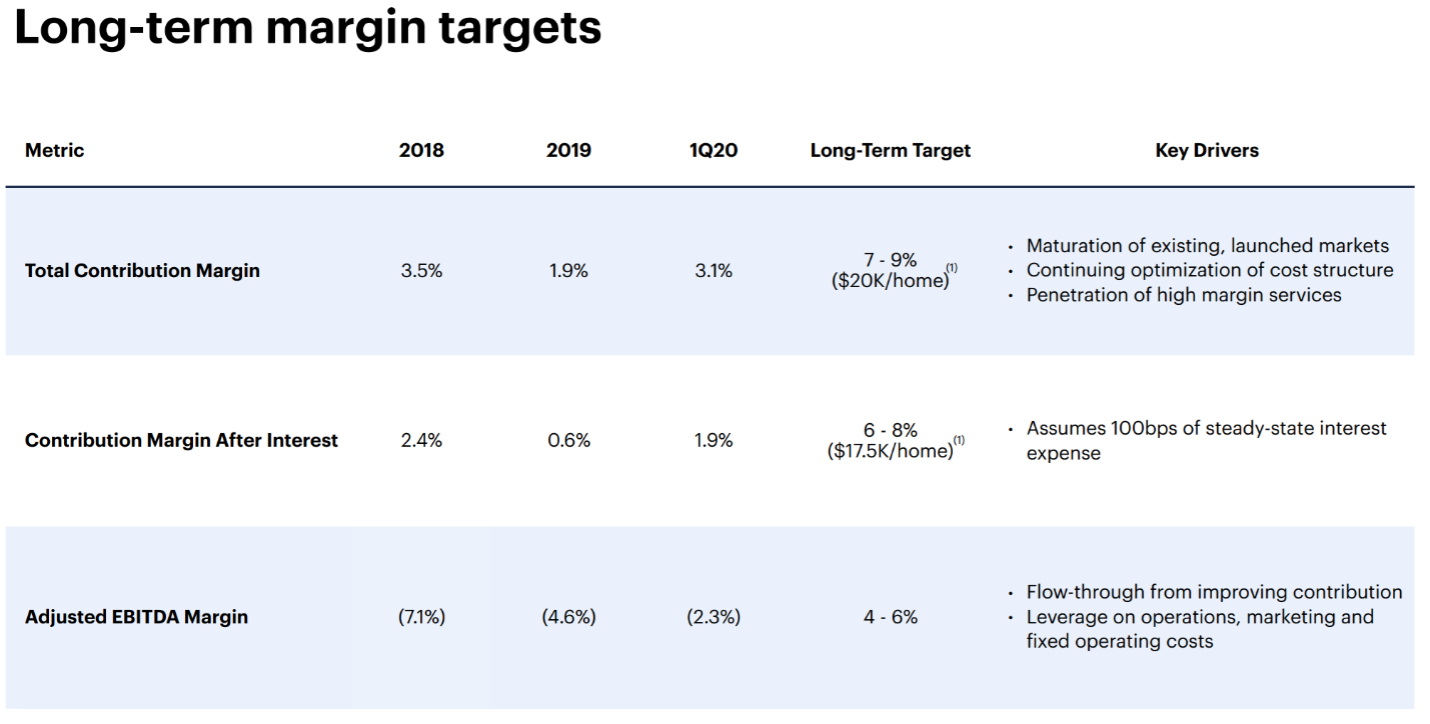

For those concerned about profits, worry not. Opendoor has positive gross and EBITDA (earnings before interest, taxes, depreciation, and amortization) margins already. And the company is still in its very early days of growth. It takes a 5% commission on every transaction and earns money via home appreciation through its typical 90-day holding period.

At scale, the company should be able to net gross margins north of 10% – driven by a mix of the commission fee and housing price appreciation. That’s very similar to what Amazon’s retail business nets on its gross margins. Economies of scale have enabled Amazon’s retail business to become very profitable. Similarly, economies of scale will enable Opendoor to be very profitable one day, too.

{kind=link}

And even in a down housing market, Opendoor has enough liquidity (over $2.5 billion in cash on the balance sheet) to weather some near-term turbulence. It’s also worth mentioning that the housing market has a very strong upward bias. It usually goes up. About once a decade, it goes down. And when that happens, the downturns tend to be very short-lived. Within a few months, the housing storm will pass. And Opendoor will be back to firing on all cylinders. So, a down housing market won’t stop this formidable company.

In fact, after recently proving the resiliency of its business model in a housing market slowdown, OPEN took flight. Though the headline numbers were mixed, they underscored that Opendoor will not lose a lot of money in this slowdown.

Opendoor Is Proving Its Resiliency

Second-quarter numbers topped estimates across the board (volumes, ASPs, revenues, earnings, and margins). Topline KPIs are slowing – volumes and ASPs dropped sequentially – and guidance came in well-below estimates. Still, the market was quite impressed with the quarter, thanks to the company’s margins.

Gross margins expanded to near record highs. EBITDA margins did reach record highs. And next quarter, EBITDA losses are expected to be very shallow, even against the backdrop rapidly slowing housing market.

In other words, the big concern with Opendoor has always been that this company will lose a lot of money in a housing market slowdown. But that’s not the case. Opendoor is simply slowing the pace of its acquisitions, focusing on high-quality inventory, and relying on its pricing algorithms to drive continued positive contribution margins and barely-negative EBITDA amid this turbulent time.

That’s really bullish. Turbulent periods in the housing market don’t last long. So, when this period ends, Opendoor is positioned to grow like wildfire for the next 10-plus years.

The Final Word

We believe this quarter is the beginning of Opendoor proving the resiliency of its business model to Wall Street. Once Wall Street is fully convinced – maybe another quarter or two of outperformance in a down housing market – this stock will fly higher.

We’re pounding the table on this stock as a multi-bagger with 10X potential.

And in all honesty, there are other stocks on my radar with even higher upside potential — much higher.

That’s why I want to share the name, ticker symbol, and key business details of my No. 1 space stock to buy right now.

It’s a tiny, hyper-innovative company using space-based technologies to fix the world’s biggest problem: slow and inconsistent internet connections.

And this explosive stock stands out among that group of superstars for having up to 100X upside potential…

In just a few weeks, this company will perform the most important launch since July 1969. If it’s successful, it will change the world as we know it. And its stock could rocket 10X over the next month alone.

Who knows? Maybe you could use this investment to one day join the billionaire class.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.