Crises create opportunities.

Take the tech crisis in the early 2000s, for example. The dot-com crash of 2000 bankrupted countless internet startups, including dozens of e-commerce companies like Boo.com, Pets.com, and Webvan.

But one tiny firm named Amazon (AMZN) emerged as a resilient winner in the e-commerce space, even as its online retail peers kept dropping like flies.

The result? All the customers that were shopping at those failed e-commerce startups migrated to Amazon.com. Its website remained up-and-running, the costs were low, and the shipping remained second-to-none.

Essentially, Amazon ate up the entire e-commerce category.

Over the next 20 years, as the e-commerce space continued to grow, Amazon’s user base, revenues, and profits did the same.

And its stock went parabolic.

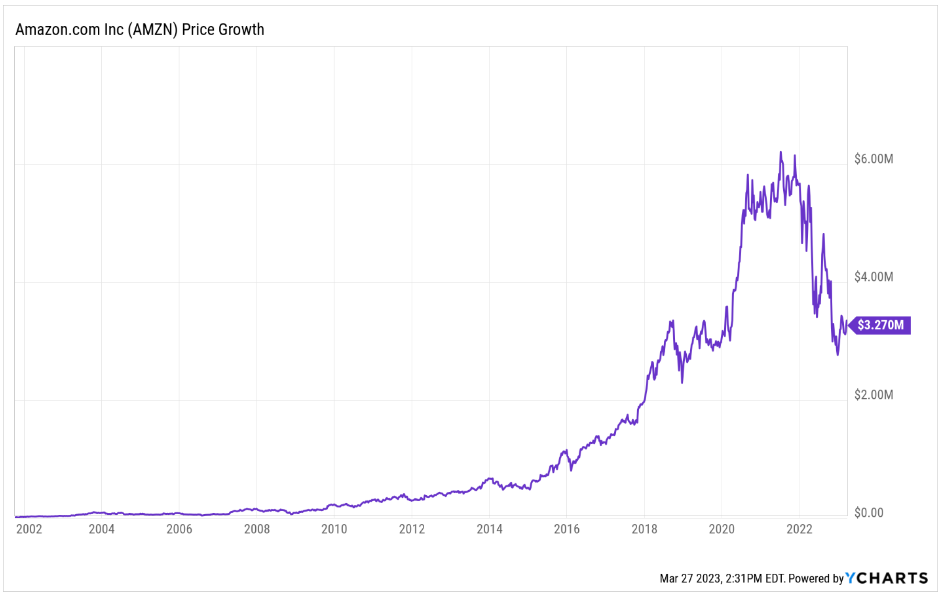

Every $10,000 invested in AMZN stock at its low during the dot-com crash would be worth more than $3.2 million today!

{kind=link}

Alas, I repeat: Crises create opportunities. The bigger the crisis, the bigger the opportunity.

And currently, we have a major banking crisis on our hands.

Profit From the Banking Crisis

Over the past three weeks alone, four major banks – Silicon Valley Bank, Signature Bank, Credit Suisse (CS), and First Republic (FRC) – have either failed or nearly failed.

It’s the biggest financial crisis this country has seen since 2008 – and, before that, the Great Depression.

As a result, most bank stocks are now crashing.

But in the midst of all this chaos, one small bank is emerging as the potential “Amazon of Finance.”

It is a small neobank that is showing significant and impressive signs of strength at the same time that many of its peers are collapsing.

Unsurprisingly, while most bank stocks are crashing right now, this bank stock is rising.

And we think the ascent is just getting started.

In fact, we think buying shares of this tiny bank stock today could be like buying shares of Amazon back in early 2001. That’s because we think this neobank is about to do to the financial sector what Amazon did to e-commerce 20 years ago: consolidate it and monopolize it.

The tiny bank stock I am referring to? None other than SoFi Technologies (SOFI).

Banks Suck, But SoFi Solves the Problem

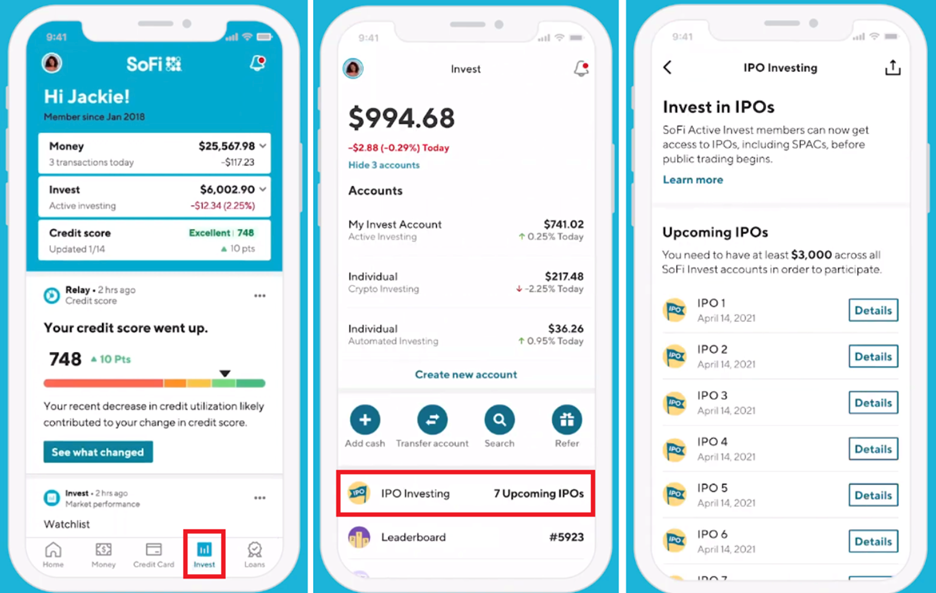

Forget physical banking. SoFi is creating a new generation of digitally-native online banking made for the modern consumer, all through a single “super app.”

Basically, SoFi is trying to do to Bank of America (BAC) and Wells Fargo (WFC) what Amazon did to JCPenney and Sears, hence the “Amazon of Finance” title.

And we believe it will be successful in these efforts, primarily for one simple reason: Hardly anyone likes the legacy banking process.

Account fees. Clearinghouses. High interest rates. Broken digital platforms. Confusing rewards programs. Long phone calls and in-person appointments. The whole process is slow, expensive, and cumbersome. That’s mostly because the industry is full of profit-taking middlemen and rooted in antiquated and costly physical processes.

So… what if technology automated out those middlemen profit-takers? What if someone created an entirely digital bank, with all technology-driven processes that delivered fast, cheap, and convenient financial solutions to customers all across America? Better yet, what if someone did all that, and then put it all into an app, allowing you to control all your banking from your phone?

That’s what SoFi is doing.

The SoFi Origin Story

SoFi was founded in 2011 by Stanford business school students who were fed up with the inefficiency of the student loan financing industry. They saw a huge opportunity to fix those inefficiencies, which they recognized were rooted in two things.

At the time, banking was a physical-first industry and, therefore, was weighed down by lots of property-related expenses that were inevitably passed on to the consumer.

Secondly, student loans were typically structured as complex transactions with tons of middle-men, all of whom had their own fee that the college student had to pay.

SoFi was created, on the idea that the platform could leverage automated technologies and a digitally-native experience to create hyper-convenient access to cheap student loan refinancing.

It worked.

SoFi’s “Super App”

Over the past decade, students across America have flocked to refinance their loans through SoFi to take advantage of their lower rates, which have been achieved through the use of technology to reduce the operating costs of the business. (And SoFi has, of course, passed those cost-savings on to its customers.)

That was the “hero product” that put SoFi on the map in the fintech world.

SoFi has since leveraged this success story to build an ecosystem of high-quality, low-cost, and hyper-convenient fintech solutions – all of which are accessible through a single, intuitive “super app.”

{kind=link}

Through the SoFi app, the company offers:

- SoFi Money: a cash management account that acts like a mobile checking or savings account. It has no account fees, 1% APY and an attached debit card.

- SoFi Invest: an attached mobile investing account. In it, consumers can use their funds from SoFi Money to invest in stocks, ETFs and cryptocurrencies. They can also invest in pre-IPO shares, which are usually reserved for institutional clients.

- SoFi Credit Card: an attached credit card. Consumers can link their Money accounts to this card and earn 2% cash-back on all purchases. Those rewards can be used to pay down debt through a SoFi loan or invest in stocks/cryptos with SoFi Invest. And there’s no annual fee.

- SoFi Relay: an attached budgeting software tool. Consumers can use it to track and monitor spending via SoFi accounts and external linked bank accounts. They can also check their credit score.

- SoFi Education: complementary educational articles and videos that help consumers learn everything about finance. It covers topics from how to invest in cryptos, to what an APR is, to why credit scores matter.

With SoFi, you get all of that… in one application. Its all-in-one mobile money app is leveraging technology to make banking fast, cheap, and easy.

It is the future. And right now, that future is becoming crystal clear because of SoFi’s strength amidst the recent banking crisis.

SoFi Is Showing Strength in the Banking Crisis

The current banking crisis is all about deposit insurance.

Long story short, banks made some bad bets on the direction of interest rates in 2020 and ‘21. Since interest rates have soared over the past 12 months, many of them now do not have the funds to cover withdrawals if a bunch of customers start pulling their money.

At most banks, the FDIC only insures up to $250,000. Therefore, in a scenario where a bank runs out of money in a classic “bank run” – like what happened at Silicon Valley Bank – customers could lose every dollar over $250,000 that they had in that bank.

It’s spooky stuff.

As a result, we’ve seen huge outflows from small bank accounts over the past few days. And those regional banks have been struggling to scrape together enough cash to fund all those outflows.

But guess what’s happening over at SoFi?

No panic, no stress, no worries.

Instead, the company just announced an industry-first during this crisis: FDIC insurance on funds up to $2 million!

In pretty much every other bank account across America, you are only insured by the federal government on funds up to $250,000. But because SoFi has developed an ingenious insurance network with other banks, your money at SoFi is now insured up to $2 million – 8X the national average!

SoFi isn’t struggling through this crisis. It’s surging through it…

Much like Amazon surged through the e-commerce crisis of the early 2000s.

We see the writing on the wall here. The “Amazon of Finance” is emerging in the banking crisis, and that company is SoFi.

It’s turning crisis into opportunity – and it is creating a generational investment opportunity for you and me.

The Final Word

Crisis creates opportunity. History is crystal clear on that.

History is also crystal clear on the fact that fortune favors the bold. And in financial markets, that means fortune favors those who capitalize on the opportunities created by crises.

Right now, you have one such opportunity. The banking sector is in meltdown mode. But this is not the end of banks. It’s the end of the old banks – and the start of a new generation of banks.

SoFi is the leader in this new generation of banks. It is the emerging “Amazon of Finance.”

Investors who bought the dip in Amazon stock at its dot-com-crash lows have since turned every $10,000 into more than $3.2 million. Similar returns look entirely possible with dip-buyers on SoFi stock today.

That’s why SoFi stock may be the best opportunity out there today.

Actually… let me take that back…

There is one other growth stock out there that offers even more upside potential than SoFi stock at current levels. And we think it represents an even better buying opportunity.

Why? Because this stock is building the groundbreaking technology that the future of the banking industry will be built on top of.

It’s also the groundbreaking technology that the cybersecurity industry will be built on top of… and the digital media industry… the telecom industry… the defense industry… the cloud computing industry… and pretty much every other industry, too.

It is a singular technology that could, quite literally, change everything about everything.

That’s why some investors are calling this tech more important than the invention of fire and even the wheel.

And one tiny company is building the best version of it right now.

Want to hear more about that company and its potential 100X stock? I thought so. Click here to learn more.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.